This article looks at Working Capital Management SME's.

Overview

Working capital (“WC”) is the lifeblood of business.

Poor working capital management has caused many businesses to stagnate or fail completely, despite having solid business models.

Key Components of WC?

A technical definition is the capital of a business which is used in its day-to-day operations, calculated as Current Assets minus Current Liabilities. More specifically, the key components are:

-

Accounts Receivables (Debtors)

-

Inventory (Stock)

- Accounts Payable (Creditors)

Reviewing you WC?

Firstly, no amount of efficient WC can be a substitute for a good business model and sufficient Gross Margins. This is the foundation of your Profit & Loss.

WC management has a greater impact on your Cash position.

It is important to assess the performance of all key WC classes. It will tell a lot about the operational efficiency of most businesses.

Let’s use an example of a wholesale business, WCM 1.

This business is growing, reflected in increased sales and purchases of inventory.

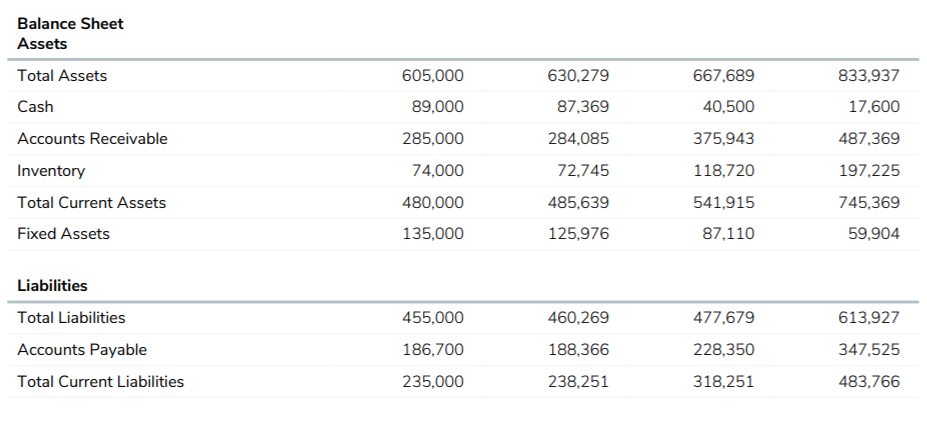

A review of both historical, current and projected performance showed the following WC position:

This represented Net Working Capital at the end of FY 21 of $337,000.

The business had pursued a path of growth, had acquired more customers, grown revenue substantially and Profits marginally; however, after a couple of years had found itself short of cash. Accounts Payable terms were also beginning to stretch out, and the business was constantly managing supplier requests for payment.Typically, businesses that are growing like this reach out for more capital contribution or debt. This is an example of where short term funders have flourished; however, the business paused to review its progress.

Measuring your Working Capital Cycle

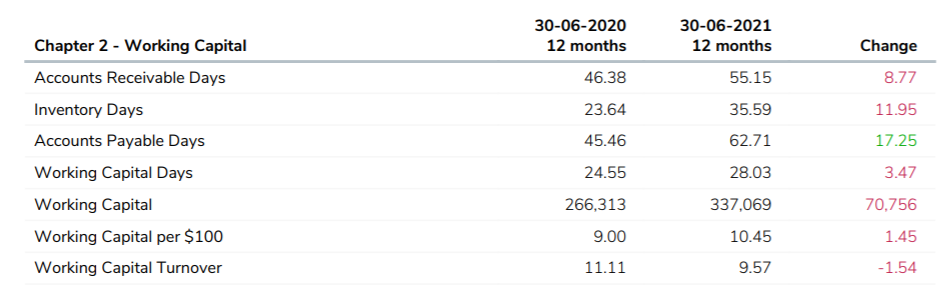

Net Working Capital had grown, and the data was examined further as below:

Source: Cashflow Story - www.cashflowstory.com.au

The Business Review noted:

Accounts Receivable Days had adversely increased by 9 days.

Inventory Days had adversely increased by 12 days.

Accounts Payable had pushed out by over 17 days.

Working Capital Days (Defined as Debtor Days + Inventory Days - Accounts Payable Days) and Working Capital Turnover (Defined as Revenue / Total WC) had also deteriorated materially.

WCM1 identified that it could improve its WC management, rather than borrowing to manage working capital gaps.

Remediation Steps

To achieve this, WCM1 put the following in place:

-

Refocused on its Customer collections.

-

Decided to exit a customer that had 120 average payment days and lower than average gross margin.

-

Reviewed its slow performing inventory lines, made some write downs and decided to exit some small selling products.

-

Renegotiated some supplier terms and them committed to meeting payments on time.

-

Reviewed its Sales discounting policy to improve Gross margins.

This caused some short term pain, including no distribution of profits, though within six months the business was much stronger.

It is a reminder that a key to success is to combine good WC management, with a sound business model & and a sustained gross margin.

More Information?

E - info@clefinance.com.au

W - clefinance.com.au